Attorney-Verified Loan Agreement Template for California

Attorney-Verified Loan Agreement Template for California

Free Promissory Note Template Florida - Signatures from both parties validate the agreement legally.

Choosing a trusted individual to act on your behalf is essential, and the Durable Power of Attorney form is an effective way to ensure your wishes are respected when you are unable to communicate them yourself. This document empowers your designated agent to manage critical decisions regarding your finances and healthcare, providing security for you and your loved ones during challenging times.

Promissory Note New York - All personal and financial details required by the lender should be provided in the Agreement.

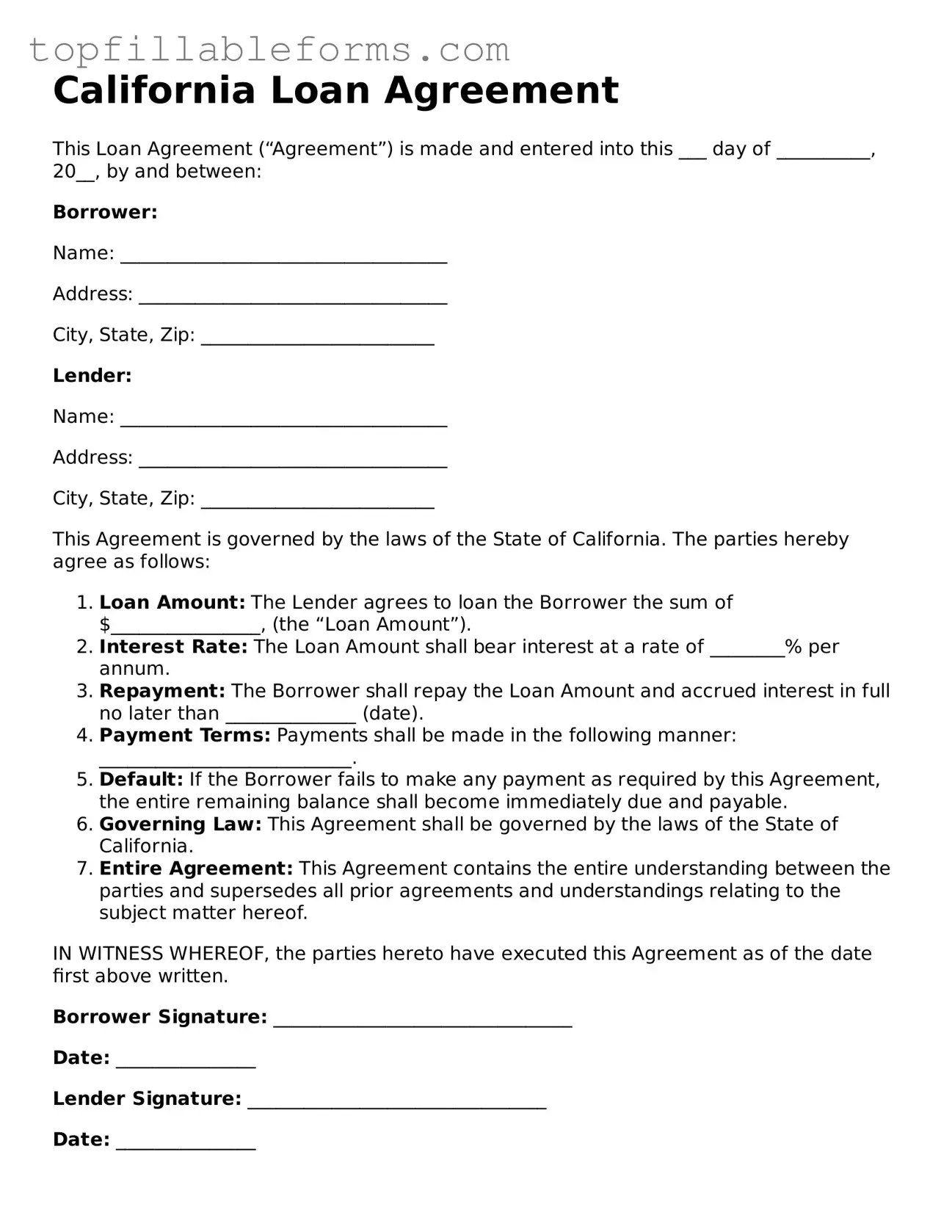

California Loan Agreement

This Loan Agreement (“Agreement”) is made and entered into this ___ day of __________, 20__, by and between:

Borrower:

Name: ___________________________________

Address: _________________________________

City, State, Zip: _________________________

Lender:

Name: ___________________________________

Address: _________________________________

City, State, Zip: _________________________

This Agreement is governed by the laws of the State of California. The parties hereby agree as follows:

IN WITNESS WHEREOF, the parties hereto have executed this Agreement as of the date first above written.

Borrower Signature: ________________________________

Date: _______________

Lender Signature: ________________________________

Date: _______________

When engaging in a loan agreement in California, several additional documents may accompany the primary agreement to ensure clarity and legal compliance. Each of these documents serves a specific purpose and can help protect the interests of both the lender and the borrower.

Understanding these documents can significantly enhance the borrowing experience. By being informed about each component, both lenders and borrowers can navigate the loan process with greater confidence and security.

When considering a Loan Agreement, it's helpful to understand how it relates to other financial documents. Each of these documents serves a unique purpose but shares similarities in structure and intent. Here’s a list of eight documents that are comparable to a Loan Agreement:

Doctors Excuse Note: The Doctors Excuse Note form is essential for verifying medical conditions that prevent individuals from attending work or school. For more information on obtaining this form, visit https://doctorsexcusenote.com/free-doctors-excuse-note.

Understanding these documents can help you navigate the financial landscape more effectively. Each serves a purpose, but they all aim to clarify the expectations and responsibilities of both parties involved.

Understanding the California Loan Agreement form is crucial for both lenders and borrowers. However, several misconceptions can lead to confusion. Here are ten common misunderstandings:

Being aware of these misconceptions can help individuals navigate the complexities of loan agreements more effectively.

What is a California Loan Agreement?

A California Loan Agreement is a legally binding document that outlines the terms and conditions under which a loan is provided. It specifies the amount of money being lent, the interest rate, repayment schedule, and any collateral involved. This agreement serves to protect both the lender and the borrower by clearly stating their rights and obligations.

Who can use a California Loan Agreement?

Any individual or entity involved in lending or borrowing money can utilize a California Loan Agreement. This includes private lenders, financial institutions, businesses, and personal loans between friends or family members. However, it is essential that both parties fully understand the terms before signing the agreement to avoid potential disputes.

What key elements should be included in the agreement?

A comprehensive California Loan Agreement should include the following elements:

Including these elements ensures clarity and minimizes misunderstandings between the parties involved.

Is it necessary to have a lawyer review the Loan Agreement?

While it is not legally required to have a lawyer review a California Loan Agreement, doing so is highly advisable. A legal professional can help ensure that the document complies with state laws and protects your interests. They can also identify any potential pitfalls or ambiguities in the agreement that could lead to future disputes.

What happens if one party defaults on the loan?

If a borrower defaults on the loan, the lender has several options available. The specific actions that can be taken depend on the terms outlined in the Loan Agreement. Common remedies include charging late fees, initiating collection procedures, or pursuing legal action to recover the owed amount. The agreement should clearly outline the steps that will be taken in the event of default to avoid confusion.

Can the terms of the Loan Agreement be modified after it has been signed?

Yes, the terms of a California Loan Agreement can be modified after it has been signed, but this typically requires mutual consent from both parties. Any changes should be documented in writing and signed by both the lender and the borrower to ensure that the modifications are legally enforceable. Oral agreements regarding changes may not hold up in court, so it is best to formalize any amendments in writing.