Attorney-Verified Promissory Note Template for California

Attorney-Verified Promissory Note Template for California

Texas Promissory Note - It is important for both parties to understand their rights and obligations within the note.

For those looking to ensure a legal transfer of ownership, our guide to the important Motorcycle Bill of Sale document outlines the necessary steps and information required in Washington State.

Create Promissory Note - Repayment schedules can vary widely based on agreements between the parties.

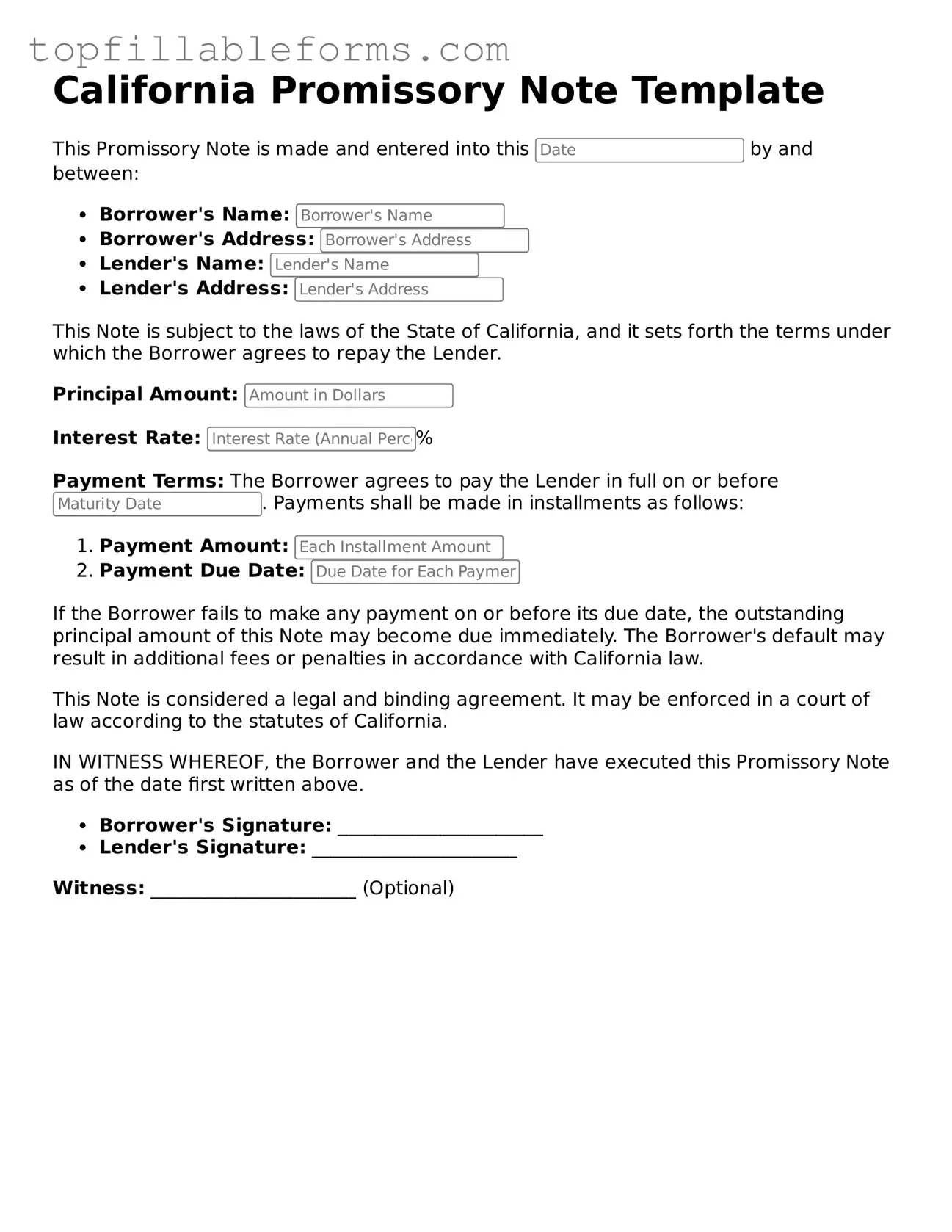

California Promissory Note Template

This Promissory Note is made and entered into this by and between:

This Note is subject to the laws of the State of California, and it sets forth the terms under which the Borrower agrees to repay the Lender.

Principal Amount:

Interest Rate: %

Payment Terms: The Borrower agrees to pay the Lender in full on or before . Payments shall be made in installments as follows:

If the Borrower fails to make any payment on or before its due date, the outstanding principal amount of this Note may become due immediately. The Borrower's default may result in additional fees or penalties in accordance with California law.

This Note is considered a legal and binding agreement. It may be enforced in a court of law according to the statutes of California.

IN WITNESS WHEREOF, the Borrower and the Lender have executed this Promissory Note as of the date first written above.

Witness: ______________________ (Optional)

When engaging in a loan agreement in California, a Promissory Note is often accompanied by various other documents that help clarify the terms and protect the interests of both parties. Understanding these documents can enhance the overall transaction and ensure compliance with legal standards.

Each of these documents plays a crucial role in the lending process, ensuring clarity and legal protection for both parties involved. Familiarity with these forms can facilitate smoother transactions and help avoid potential disputes.

A Promissory Note is a financial document that outlines a promise to pay a specific amount of money to a designated party under agreed-upon terms. Several other documents share similarities with a Promissory Note, each serving unique purposes while maintaining fundamental characteristics. Below are ten such documents:

Understanding these documents can help individuals and businesses navigate their financial obligations more effectively. Each serves a distinct purpose, yet they all share the fundamental principle of establishing a promise to pay.

Understanding the California Promissory Note form is essential for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion. Here are five common misconceptions:

By addressing these misconceptions, borrowers and lenders can navigate the use of promissory notes with greater confidence and understanding.

A California Promissory Note is a written agreement between a borrower and a lender. It outlines the terms of a loan, including the amount borrowed, interest rate, repayment schedule, and any other conditions agreed upon by both parties. This document serves as a legal record of the debt.

The key components typically include:

Yes, a Promissory Note is a legally binding document. Once signed by both parties, it creates an obligation for the borrower to repay the loan according to the terms outlined in the note. If the borrower fails to meet these terms, the lender has the right to take legal action.

While it is not legally required to have a lawyer draft a Promissory Note, consulting with one can be beneficial. A lawyer can help ensure that the document meets all legal requirements and adequately protects your interests.

Yes, a Promissory Note can be modified, but both parties must agree to the changes. It is advisable to document any modifications in writing and have both parties sign the revised agreement to avoid misunderstandings in the future.

If the borrower defaults, the lender can take several actions. This may include demanding full payment of the remaining balance, charging late fees, or pursuing legal action to recover the owed amount. The specific actions depend on the terms of the Promissory Note and applicable state laws.

Templates for California Promissory Notes can be found online through various legal document websites. It is important to ensure that the template complies with California laws and includes all necessary components to be enforceable.