Attorney-Verified Loan Agreement Template for Florida

Attorney-Verified Loan Agreement Template for Florida

California Promissory Note Template - The Loan Agreement may specify permitted uses for the funds.

Free Promissory Note Template Texas - The document will outline any fees associated with the loan processing.

The Washington Employment Verification form is crucial for lending institutions and property managers. For those looking to streamline their applications, understanding the nuances of the comprehensive Employment Verification process can greatly enhance efficiency and success.

Promissory Note New York - The Loan Agreement can protect the borrower by clearly defining terms.

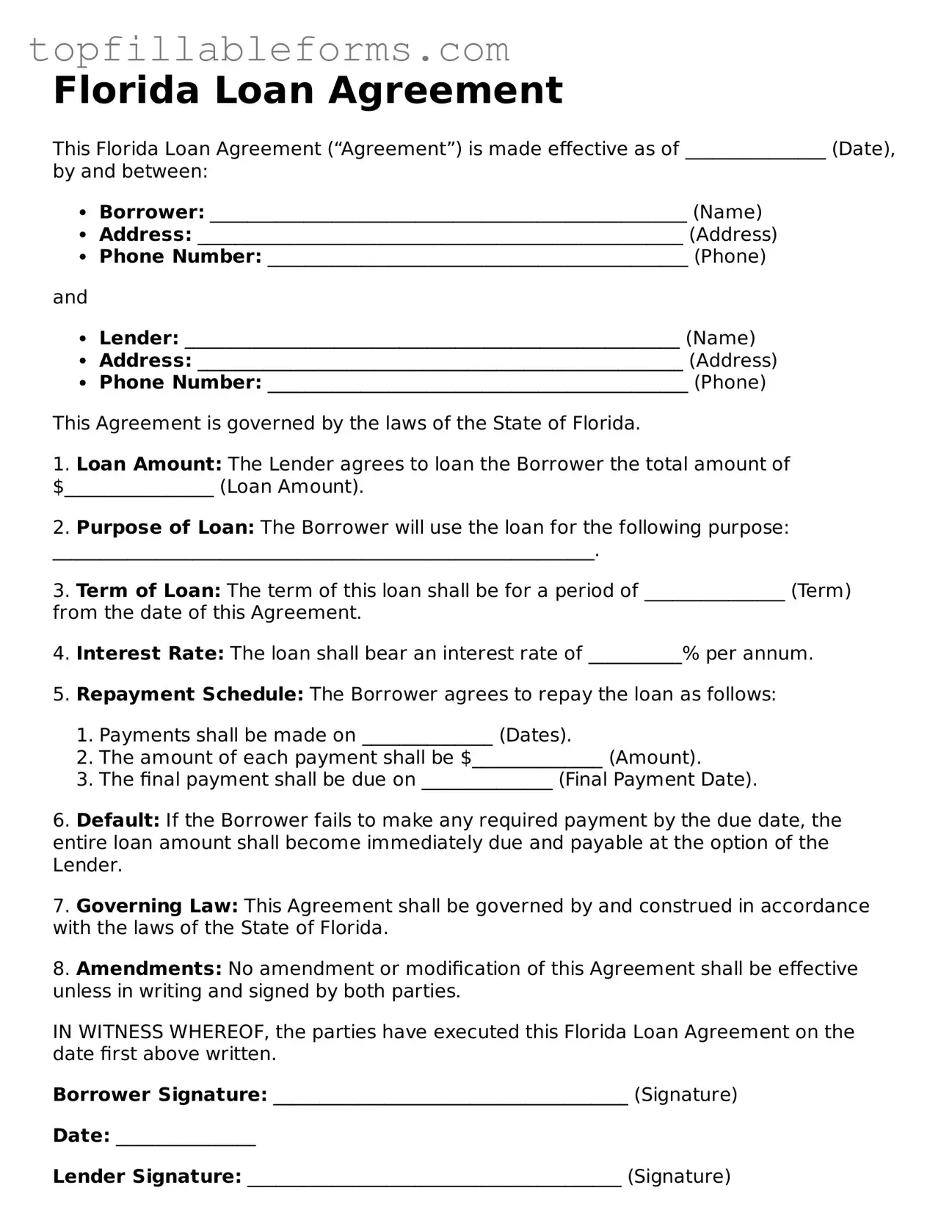

Florida Loan Agreement

This Florida Loan Agreement (“Agreement”) is made effective as of _______________ (Date), by and between:

and

This Agreement is governed by the laws of the State of Florida.

1. Loan Amount: The Lender agrees to loan the Borrower the total amount of $________________ (Loan Amount).

2. Purpose of Loan: The Borrower will use the loan for the following purpose: __________________________________________________________.

3. Term of Loan: The term of this loan shall be for a period of _______________ (Term) from the date of this Agreement.

4. Interest Rate: The loan shall bear an interest rate of __________% per annum.

5. Repayment Schedule: The Borrower agrees to repay the loan as follows:

6. Default: If the Borrower fails to make any required payment by the due date, the entire loan amount shall become immediately due and payable at the option of the Lender.

7. Governing Law: This Agreement shall be governed by and construed in accordance with the laws of the State of Florida.

8. Amendments: No amendment or modification of this Agreement shall be effective unless in writing and signed by both parties.

IN WITNESS WHEREOF, the parties have executed this Florida Loan Agreement on the date first above written.

Borrower Signature: ______________________________________ (Signature)

Date: _______________

Lender Signature: ________________________________________ (Signature)

Date: _______________

When entering into a loan agreement in Florida, several other forms and documents may be used to support the transaction. These documents help clarify the terms and provide necessary information to both parties involved. Below is a list of commonly used forms associated with a Florida Loan Agreement.

These documents play a crucial role in the loan process, providing clarity and protection for both the borrower and lender. Understanding each document's purpose can help ensure a smoother transaction.

Promissory Note: This document outlines the borrower's promise to repay a loan. Like a Loan Agreement, it includes details about the loan amount, interest rate, and repayment schedule.

Mortgage Agreement: A Mortgage Agreement secures a loan with property as collateral. Similar to a Loan Agreement, it specifies the terms of the loan and the responsibilities of both parties.

Credit Agreement: This document governs the terms of a credit facility, such as a line of credit. It shares similarities with a Loan Agreement in detailing the amount, interest rates, and repayment terms.

Lease Agreement: A Lease Agreement outlines the terms for renting property. While it focuses on rental terms, it also includes payment schedules, similar to how a Loan Agreement specifies loan repayment.

Durable Power of Attorney: The Arizona Durable Power of Attorney form is a legal document that allows an individual, known as the principal, to grant another person the authority to make decisions on their behalf. This power remains effective even if the principal becomes incapacitated. It's a tool designed for planning ahead, ensuring that the individual's affairs can be managed according to their wishes if they're unable to do so themselves. More information can be found here: Durable Power of Attorney.

Personal Loan Agreement: This is a specific type of Loan Agreement for personal loans. It details the amount borrowed, interest rates, and repayment terms, just like a standard Loan Agreement.

Understanding the Florida Loan Agreement form is crucial for borrowers and lenders alike. However, several misconceptions can lead to confusion. Here are six common misconceptions:

Many people believe that all loan agreements follow a standard format. In reality, each agreement can vary significantly based on the lender's requirements and the specific terms negotiated.

Some borrowers think that once they sign a loan agreement, the terms are set in stone. However, terms can often be renegotiated before the loan is finalized, depending on the lender's policies.

This form can be used for various loan amounts, not just large sums. Whether it's a small personal loan or a larger mortgage, the form is applicable.

Different lenders may have varying documentation requirements. Borrowers should check with their specific lender to understand what is needed for their loan application.

While many loans have fixed rates, some loans may have variable rates that can change over time. It is essential to clarify this before signing.

In fact, a well-drafted loan agreement protects both parties. It outlines the rights and responsibilities of both the borrower and the lender, ensuring fairness in the transaction.

A Florida Loan Agreement is a legal document that outlines the terms and conditions of a loan between a lender and a borrower in the state of Florida. This agreement specifies the amount of money being borrowed, the interest rate, repayment schedule, and any collateral involved. It serves to protect both parties by clearly defining their rights and responsibilities.

Any individual or business in Florida can use a Loan Agreement. This includes personal loans between friends or family members, as well as more formal arrangements between businesses and lenders. It is important that both parties understand the terms and agree to them before signing the document.

A comprehensive Loan Agreement should include:

Including these details helps prevent misunderstandings and disputes in the future.

Yes, once both parties sign the Loan Agreement, it becomes a legally binding contract. This means that both the lender and borrower are obligated to adhere to the terms outlined in the agreement. If either party fails to comply, the other party may have the right to pursue legal action to enforce the agreement or seek damages.