Free Loan Agreement Form

Free Loan Agreement Form

Taxs - Engaging with the IRS online can provide additional support for 1040 inquiries.

A Georgia Durable Power of Attorney form is a legal document that grants an individual the authority to make decisions on behalf of another person. This arrangement remains effective even if the person who created it becomes incapacitated. Understanding how this form works can greatly benefit individuals seeking to ensure their financial and medical affairs are handled according to their wishes, and you can find the necessary document by accessing the Durable Power of Attorney form.

Media Release Form - This document can detail any potential risks associated with the use of the individual’s likeness.

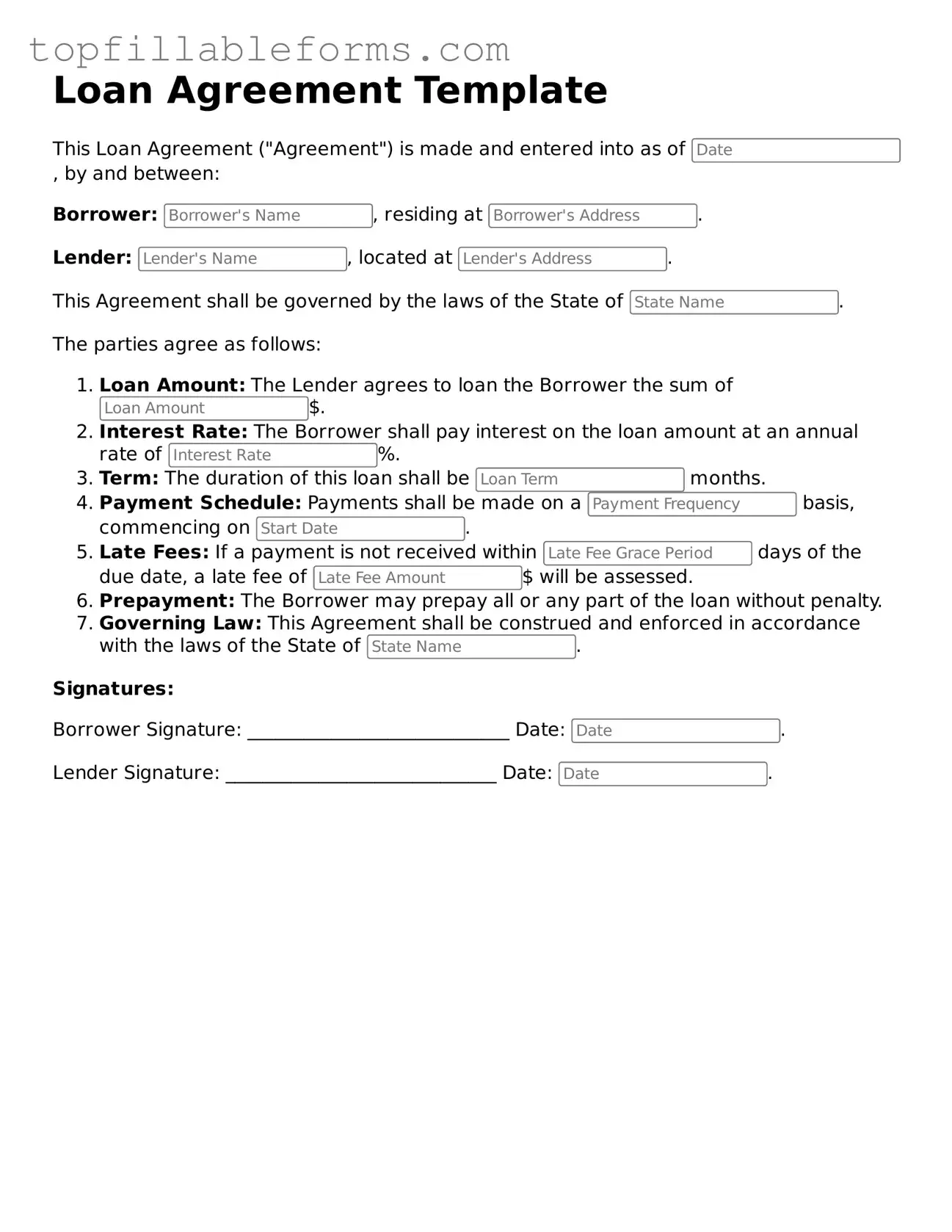

Loan Agreement Template

This Loan Agreement ("Agreement") is made and entered into as of , by and between:

Borrower: , residing at .

Lender: , located at .

This Agreement shall be governed by the laws of the State of .

The parties agree as follows:

Signatures:

Borrower Signature: ____________________________ Date: .

Lender Signature: _____________________________ Date: .

When entering into a Loan Agreement, several other documents may be necessary to ensure a smooth transaction. Each of these forms serves a specific purpose and helps clarify the terms of the loan, protecting both the lender and the borrower. Below is a list of commonly used documents that often accompany a Loan Agreement.

Having these documents in place can help ensure clarity and security for both parties involved in the loan process. By understanding the purpose of each document, borrowers and lenders can navigate their agreement with confidence.

Loan agreements are important documents that outline the terms and conditions of borrowing money. However, there are several misconceptions about them that can lead to confusion. Here are nine common misconceptions:

Understanding these misconceptions can help individuals navigate the borrowing process more effectively and ensure that their rights are protected.

A Loan Agreement is a legally binding document between a borrower and a lender. It outlines the terms and conditions under which money is borrowed and specifies the repayment schedule, interest rates, and any collateral involved. This agreement serves to protect both parties by clearly defining their rights and obligations.

A comprehensive Loan Agreement typically includes:

Including these elements helps ensure clarity and reduces the potential for disputes in the future.

To ensure that a Loan Agreement is enforceable, it is important to follow these guidelines:

By adhering to these practices, you can help safeguard the agreement’s validity.

If the borrower defaults, the lender has several options, which may include:

It is advisable for both parties to communicate openly to resolve any issues before they escalate.