Printable Mortgage Statement Form in PDF

Printable Mortgage Statement Form in PDF

Lyft Rideshare Inspection Form - Examine the vehicle's interior for cleanliness and any damage.

Waiver of Lien to Date Chicago Title Pdf - It serves as a protection for property owners, confirming that no outstanding claims exist from the contractors involved.

The importance of having a trusted individual manage your financial affairs cannot be understated, which is why preparing a Durable Power of Attorney is essential for anyone seeking stability and security in uncertain times. This document not only grants authority to a designated agent but also ensures that your wishes are respected when you are unable to make decisions yourself.

2b Mindset Tracker - Utilize the tracker as a personal diary for food.

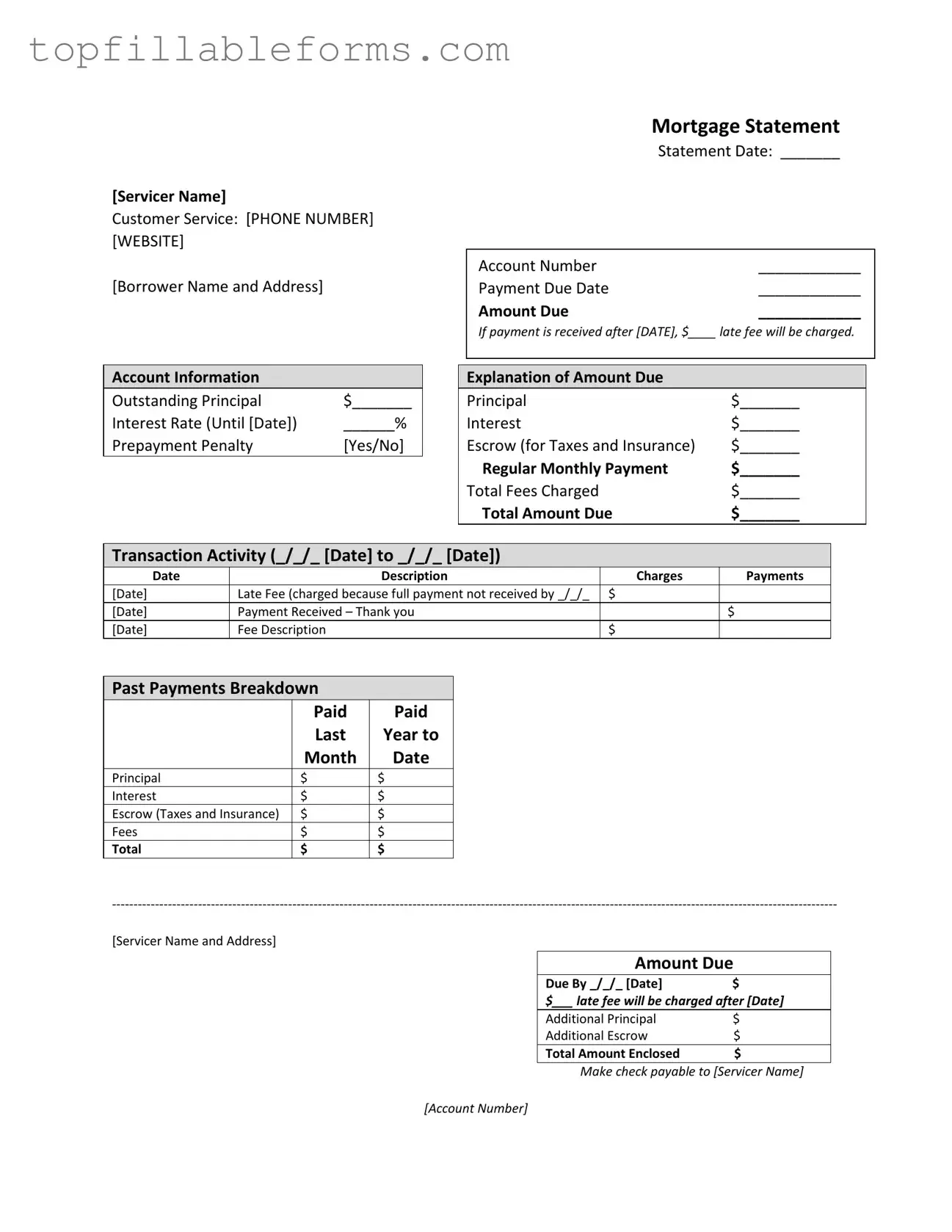

[Servicer Name]

Customer Service: [PHONE NUMBER] [WEBSITE]

[Borrower Name and Address]

Mortgage Statement

Statement Date: _______

Account Number |

____________ |

Payment Due Date |

____________ |

Amount Due |

____________ |

If payment is received after [DATE], $____ late fee will be charged.

Account Information

Outstanding Principal |

$_______ |

Interest Rate (Until [Date]) |

______% |

Prepayment Penalty |

[Yes/No] |

Explanation of Amount Due

Principal |

$_______ |

Interest |

$_______ |

Escrow (for Taxes and Insurance) |

$_______ |

Regular Monthly Payment |

$_______ |

Total Fees Charged |

$_______ |

Total Amount Due |

$_______ |

Transaction Activity (_/_/_ [Date] to _/_/_ [Date])

Date |

Description |

Charges |

Payments |

[Date] |

Late Fee (charged because full payment not received by _/_/_ |

$ |

|

[Date] |

Payment Received – Thank you |

|

$ |

[Date] |

Fee Description |

$ |

|

Past Payments Breakdown

|

Paid |

Paid |

|

Last |

Year to |

|

Month |

Date |

Principal |

$ |

$ |

Interest |

$ |

$ |

Escrow (Taxes and Insurance) |

$ |

$ |

Fees |

$ |

$ |

Total |

$ |

$ |

[Servicer Name and Address]

Amount Due

Due By _/_/_ [Date]$

$___ late fee will be charged after [Date]

Additional Principal |

$ |

Additional Escrow |

$ |

Total Amount Enclosed |

$ |

Make check payable to [Servicer Name]

[Account Number]

[Additional tables to be translated]

Important Messages

*Partial Payments: Any partial payments that you make are not applied to your mortgage, but instead are held in a separate suspense account. If you pay the balance of a partial payment, the funds will then be applied to your mortgage.

**Delinquency Notice**

You are late on your mortgage payments. Failure to bring your loan current may result in fees and foreclosure – the loss of your home. As of [Date], you are __ days delinquent on your mortgage loan.

Recent Account History

·Payment due [Date]: Fully paid on time

·Payment due [Date]: Fully paid on [Date]

·Payment due [Date]: Unpaid balance of $________

·Current payment due [Date]: $_______

·Total: $_______ due. You must pay this amount to bring your loan current.

If you are Experiencing Financial Difficulty: See back for information about mortgage counseling or assistance.

When managing a mortgage, several important documents accompany the Mortgage Statement form. Each of these documents plays a crucial role in understanding your mortgage and ensuring you stay informed about your financial obligations. Below is a list of commonly used forms and documents.

Understanding these documents can empower homeowners to manage their mortgages effectively. Being informed helps in making timely payments and addressing any issues that may arise during the life of the loan.

Billing Statement: Similar to a mortgage statement, a billing statement outlines the amounts owed for services rendered. It includes due dates, account numbers, and a breakdown of charges, ensuring clarity on what is owed and when.

Loan Statement: This document provides a summary of a loan's status, including outstanding balances, interest rates, and payment history. Like a mortgage statement, it helps borrowers understand their obligations and any fees incurred.

Credit Card Statement: A credit card statement lists transactions, outstanding balances, and due dates. It serves a similar purpose by informing the cardholder of their financial responsibilities and any applicable fees.

Utility Bill: This document details charges for services such as electricity, water, or gas. It includes amounts due, payment deadlines, and any late fees, paralleling the mortgage statement's structure.

Property Tax Bill: A property tax bill outlines the taxes owed on real estate. It specifies due dates and penalties for late payment, much like a mortgage statement, which also addresses payment deadlines and fees.

Insurance Premium Invoice: This invoice details the amount due for insurance coverage. It includes payment deadlines and any late fees, similar to the mortgage statement's function of reminding borrowers of their financial obligations.

Lease Statement: A lease statement summarizes rental payments due, including any late fees. It serves a similar role by keeping tenants informed of their payment status and obligations.

Student Loan Statement: This statement provides information on outstanding student loan balances, interest rates, and payment schedules. Like a mortgage statement, it helps borrowers keep track of their financial responsibilities.

Account Summary: An account summary provides an overview of various financial accounts, including balances, transactions, and due dates. It shares similarities with a mortgage statement in its role of summarizing important financial information.

Understanding your mortgage statement is crucial for managing your home loan effectively. However, several misconceptions often lead to confusion. Here’s a list of ten common misunderstandings regarding the mortgage statement form:

By understanding these misconceptions, homeowners can better navigate their mortgage statements and make informed decisions about their loans.

What is a Mortgage Statement?

A Mortgage Statement is a document provided by your mortgage servicer that details your mortgage account information. It includes important details such as your outstanding principal balance, interest rate, payment due date, and the total amount due for the current billing cycle. This statement helps you keep track of your payments and any fees that may apply.

What should I do if I see a late fee on my Mortgage Statement?

If you notice a late fee on your Mortgage Statement, it indicates that your payment was not received by the due date. To avoid further late fees, it’s important to make your payment as soon as possible. If you believe the late fee was charged in error, contact your mortgage servicer’s customer service for clarification and to discuss your options.

What happens if I make a partial payment?

Any partial payments you make will not be applied to your mortgage balance immediately. Instead, these funds will be held in a separate suspense account. Once you pay the remaining balance of the partial payment, those funds will then be applied to your mortgage. It’s important to make full payments to avoid complications with your account.

What should I do if I am experiencing financial difficulty?

If you are facing financial difficulties and are unable to make your mortgage payments, reach out to your mortgage servicer as soon as possible. They can provide information on mortgage counseling or assistance programs that may be available to help you manage your payments and avoid foreclosure.