Attorney-Verified Deed in Lieu of Foreclosure Template for New York

Attorney-Verified Deed in Lieu of Foreclosure Template for New York

California Voluntary Foreclosure Deed - A practical solution for homeowners looking to relieve financial burdens and start afresh.

Before signing a lease, it’s essential to review the New York Residential Lease Agreement thoroughly to ensure all terms are clear and fair, which can include referencing resources like the https://nypdfforms.com/residential-lease-agreement-form/ for additional guidance on completing the document accurately.

The Loan Servicer Might Agree to Put the Foreclosure on Hold to Give You Some Time to Sell Your Home - This way, the borrower can exit their mortgage obligation with less damage to their credit score than through foreclosure.

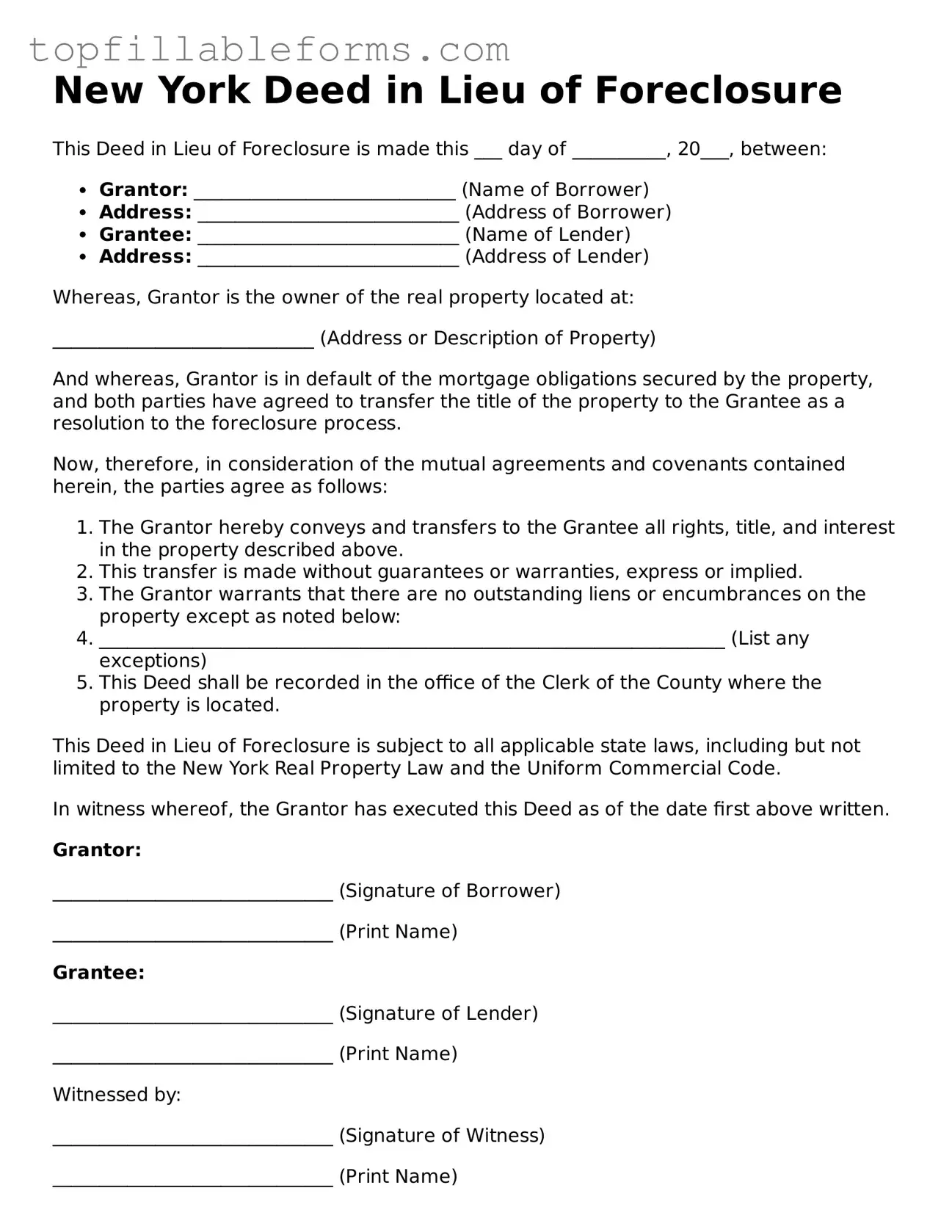

New York Deed in Lieu of Foreclosure

This Deed in Lieu of Foreclosure is made this ___ day of __________, 20___, between:

Whereas, Grantor is the owner of the real property located at:

____________________________ (Address or Description of Property)

And whereas, Grantor is in default of the mortgage obligations secured by the property, and both parties have agreed to transfer the title of the property to the Grantee as a resolution to the foreclosure process.

Now, therefore, in consideration of the mutual agreements and covenants contained herein, the parties agree as follows:

This Deed in Lieu of Foreclosure is subject to all applicable state laws, including but not limited to the New York Real Property Law and the Uniform Commercial Code.

In witness whereof, the Grantor has executed this Deed as of the date first above written.

Grantor:

______________________________ (Signature of Borrower)

______________________________ (Print Name)

Grantee:

______________________________ (Signature of Lender)

______________________________ (Print Name)

Witnessed by:

______________________________ (Signature of Witness)

______________________________ (Print Name)

Date: __________________________

When dealing with a Deed in Lieu of Foreclosure in New York, several other forms and documents may be necessary to ensure a smooth process. Each of these documents serves a specific purpose and helps clarify the rights and responsibilities of all parties involved. Below is a list of these commonly used forms.

Understanding these documents can facilitate a more efficient process when executing a Deed in Lieu of Foreclosure. Each form plays a critical role in protecting the interests of both the borrower and the lender, ensuring that all parties are aware of their rights and obligations.

Misconception 1: A Deed in Lieu of Foreclosure is the same as a short sale.

While both options allow homeowners to avoid foreclosure, they are distinct processes. A short sale involves selling the property for less than the amount owed on the mortgage, with lender approval. In contrast, a Deed in Lieu of Foreclosure transfers ownership of the property back to the lender without the need for a sale.

Misconception 2: Homeowners can simply walk away from their mortgage by signing a Deed in Lieu of Foreclosure.

This is not accurate. Homeowners must meet specific criteria and obtain lender approval before executing a Deed in Lieu. Additionally, there may be consequences, such as potential tax implications or deficiency judgments, depending on the circumstances.

Misconception 3: A Deed in Lieu of Foreclosure eliminates all debts associated with the property.

Signing this deed does not automatically erase all debts. Homeowners may still be responsible for any remaining mortgage balance or other liens on the property. It's essential to understand the financial implications before proceeding.

Misconception 4: The process is quick and straightforward.

While a Deed in Lieu of Foreclosure can be faster than a traditional foreclosure, the process still requires careful documentation and negotiation with the lender. Homeowners should expect some time and effort to finalize the arrangement.

Misconception 5: A Deed in Lieu of Foreclosure has no impact on credit scores.

This is misleading. Although it may be less damaging than a foreclosure, a Deed in Lieu can still negatively affect credit scores. Homeowners should consider the long-term effects on their credit before making a decision.

A Deed in Lieu of Foreclosure is an agreement between a homeowner and a lender. In this process, the homeowner voluntarily transfers the property title to the lender to avoid foreclosure. This option can help the homeowner avoid the lengthy and stressful foreclosure process.

There are several benefits to consider:

Eligibility typically depends on the lender’s policies. Generally, homeowners who are struggling to make mortgage payments and are facing foreclosure may qualify. However, the property must not have any liens or other claims that could complicate the transfer.

The process generally involves several steps:

Common documents include:

Yes, it can affect your credit score, but usually less severely than a foreclosure. While it may still be reported to credit agencies, the impact is often less damaging in the long term.

After the deed is transferred, the homeowner typically vacates the property. The lender may then sell the property to recover losses. Homeowners may also be able to negotiate relocation assistance from the lender.

Yes, seeking legal advice is highly recommended. An attorney can help ensure that the homeowner understands the implications of the agreement and that their rights are protected throughout the process.

If a request is denied, the homeowner should ask for the reasons behind the denial. They may also consider other options, such as loan modification or exploring short sale opportunities. Consulting with a legal professional can provide guidance on the next steps.