Attorney-Verified Loan Agreement Template for New York

Attorney-Verified Loan Agreement Template for New York

Free Promissory Note Template Texas - It may require notarization depending on the loan’s size and jurisdiction.

A Power of Attorney form in New York allows one person to grant another the authority to make decisions on their behalf. This legal document can cover a wide range of decisions, from financial matters to healthcare choices. For more information on how to obtain and complete this essential form, you can visit nypdfforms.com/power-of-attorney-form to ensure your wishes are respected in times of need.

California Promissory Note Template - The agreement typically requires signatures from all parties.

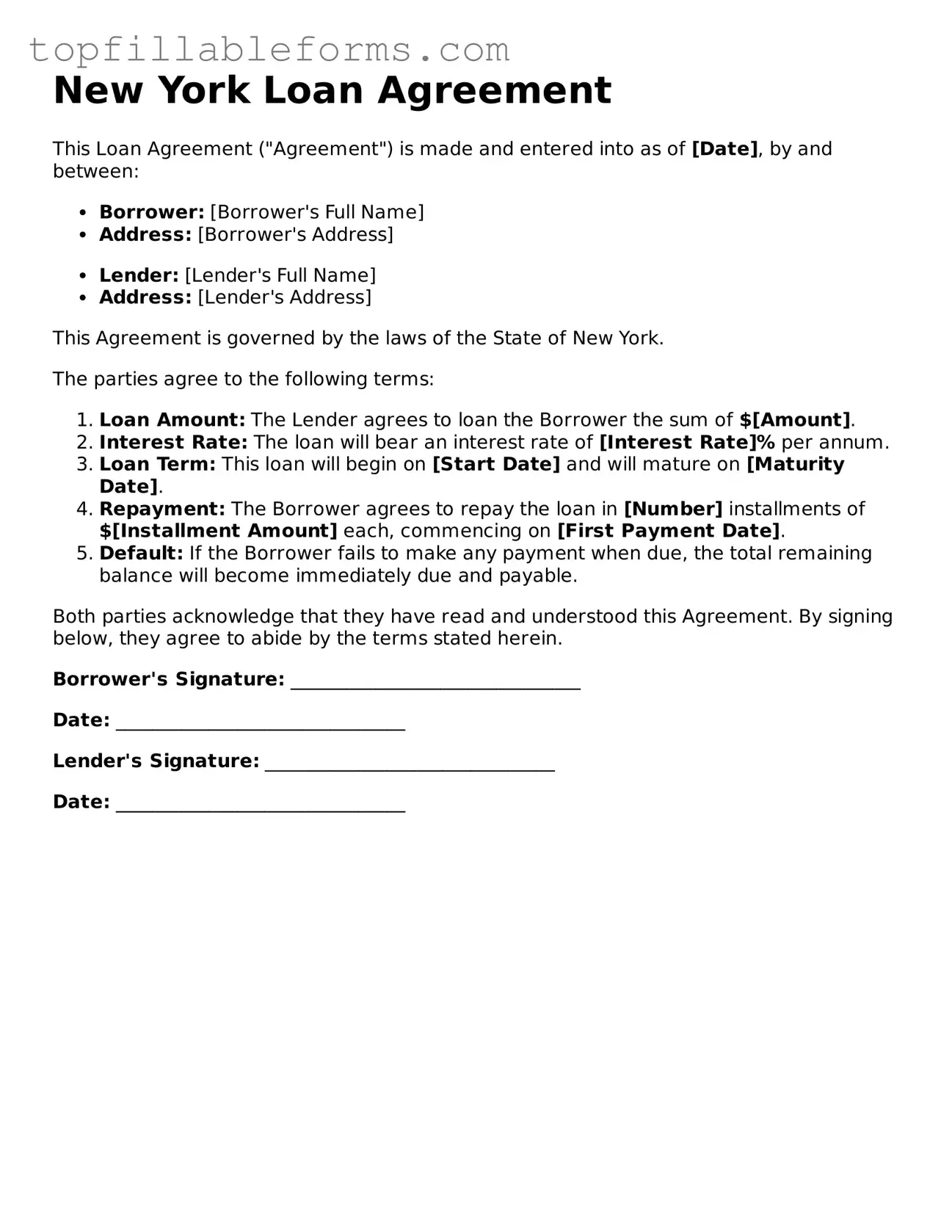

New York Loan Agreement

This Loan Agreement ("Agreement") is made and entered into as of [Date], by and between:

This Agreement is governed by the laws of the State of New York.

The parties agree to the following terms:

Both parties acknowledge that they have read and understood this Agreement. By signing below, they agree to abide by the terms stated herein.

Borrower's Signature: _______________________________

Date: _______________________________

Lender's Signature: _______________________________

Date: _______________________________

When entering into a loan agreement in New York, several other forms and documents may be necessary to ensure a smooth process. Each document serves a specific purpose and helps to clarify the terms and conditions of the loan. Below is a list of commonly used documents that complement the New York Loan Agreement form.

Understanding these documents is crucial for both lenders and borrowers. They provide clarity and protect the interests of all parties involved in the loan process. Always ensure that you have the necessary documentation in place to facilitate a successful loan agreement.

Promissory Note: A promissory note is a written promise to pay a specific amount of money at a designated time. Similar to a loan agreement, it outlines the terms of repayment and can serve as evidence of the debt.

Mortgage Agreement: This document secures a loan with real property. Like a loan agreement, it details the terms of the loan but also includes provisions about the property being used as collateral.

Credit Agreement: A credit agreement outlines the terms under which a borrower can access credit. It is similar to a loan agreement as it specifies the amount, interest rates, and repayment terms.

Trailer Bill of Sale: The California Trailer Bill of Sale form is crucial for documenting the ownership transfer of a trailer. It includes buyer and seller details, trailer specifications, and the sale price. This ensures the new owner possesses the necessary paperwork for registration. More information can be found at https://legalpdfdocs.com.

Lease Agreement: A lease agreement allows one party to use property owned by another for a specified time in exchange for payment. Both documents include terms and conditions that govern the financial relationship between parties.

Service Agreement: This document outlines the terms under which services will be provided in exchange for payment. Like a loan agreement, it specifies obligations, payment terms, and conditions for termination.

Joint Venture Agreement: This agreement is used when two or more parties agree to work together on a project. Similar to a loan agreement, it outlines the contributions, responsibilities, and financial arrangements between the parties involved.

Understanding the New York Loan Agreement form can be challenging. Here are six common misconceptions that people often have:

Being informed about these misconceptions can help you navigate the loan process more effectively.

A New York Loan Agreement form is a legal document that outlines the terms and conditions of a loan between a borrower and a lender. This agreement specifies the amount borrowed, interest rates, repayment schedule, and other important details. It serves to protect both parties by clearly stating their rights and responsibilities.

Any individual or business in New York seeking to borrow or lend money can use this form. Whether you are a private lender, a bank, or an individual looking to help a friend, this agreement is suitable for various lending situations.

The form requires basic information about both the borrower and the lender. This includes names, addresses, and contact details. Additionally, you will need to specify the loan amount, interest rate, repayment terms, and any collateral involved.

Yes, once both parties sign the agreement, it becomes a legally binding contract. This means that both the borrower and the lender are obligated to adhere to the terms outlined in the document. If either party fails to meet their obligations, the other party may have legal recourse.

If the borrower fails to repay the loan according to the agreed terms, the lender has several options. They may choose to charge late fees, negotiate new terms, or take legal action to recover the owed amount. The specific consequences should be outlined in the loan agreement.

Yes, the terms of the loan agreement can be modified, but this requires mutual consent from both parties. Any changes should be documented in writing and signed by both the borrower and the lender to ensure they are enforceable.

While it is not legally required to have a lawyer draft a loan agreement, it is often recommended. A legal professional can help ensure that the document complies with New York laws and adequately protects your interests.

You can find a New York Loan Agreement form online through various legal document websites or templates. Ensure that the form you choose is up-to-date and complies with New York state laws.