Attorney-Verified Promissory Note Template for New York

Attorney-Verified Promissory Note Template for New York

Texas Promissory Note - A Promissory Note is a written promise to pay a specified amount of money at a designated time.

Create Promissory Note - Sometimes, a co-signer may be included to guarantee payment on the note.

For a smooth homeschooling experience, parents should consider the timely submission of a "Washington Homeschool Letter of Intent" to ensure they adhere to state requirements and guidelines, which can be found on the important Washington Homeschool Letter of Intent resources.

Promissory Note Template Florida Pdf - The note may stipulate that disputes be resolved through arbitration rather than court.

California Promissory Note Requirements - This document serves as a legal record of a loan agreement between the borrower and the lender.

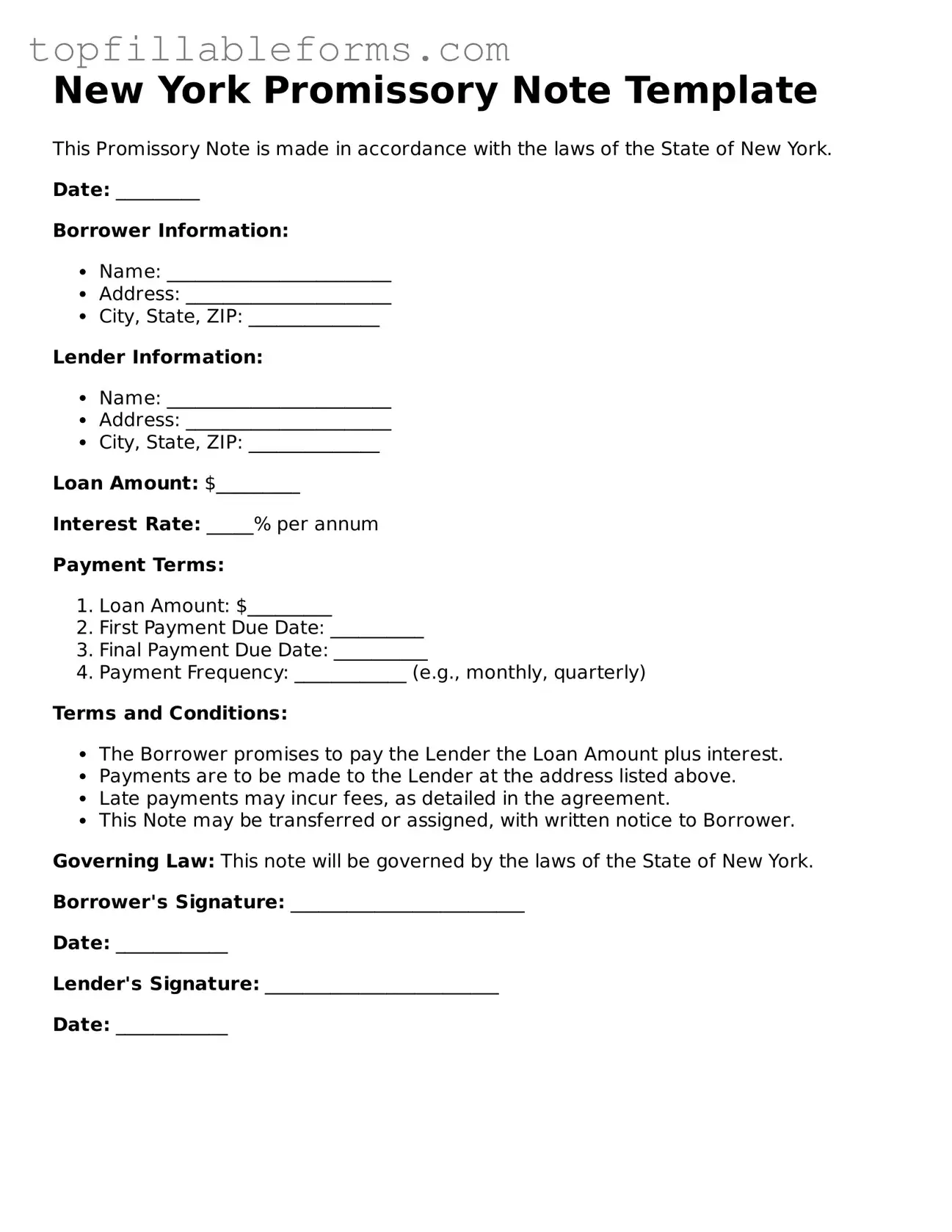

New York Promissory Note Template

This Promissory Note is made in accordance with the laws of the State of New York.

Date: _________

Borrower Information:

Lender Information:

Loan Amount: $_________

Interest Rate: _____% per annum

Payment Terms:

Terms and Conditions:

Governing Law: This note will be governed by the laws of the State of New York.

Borrower's Signature: _________________________

Date: ____________

Lender's Signature: _________________________

Date: ____________

A New York Promissory Note is a crucial document in lending transactions. However, it often works in conjunction with several other forms and documents. Understanding these related documents can help ensure a smooth lending process and protect the interests of both parties involved.

Being familiar with these documents can significantly enhance your understanding of the lending process. Each plays a vital role in ensuring that both parties are protected and informed throughout the transaction.

Understanding the New York Promissory Note form is essential for both lenders and borrowers. However, several misconceptions can lead to confusion. Here are six common misconceptions:

Clarifying these misconceptions can help individuals navigate their financial agreements with confidence.

A New York Promissory Note is a legal document in which one party, the borrower, agrees to pay a specific amount of money to another party, the lender, under agreed-upon terms. This document outlines the amount borrowed, the interest rate, payment schedule, and consequences for defaulting on the loan.

Anyone can use a Promissory Note, including individuals, businesses, and organizations. It is commonly used in personal loans, business loans, and real estate transactions. Both parties must agree to the terms laid out in the note.

A typical Promissory Note includes the following components:

Yes, a Promissory Note is legally binding as long as it meets certain requirements. Both parties must have the capacity to enter into a contract, and the terms must be clear and specific. If one party fails to meet the terms, the other party can take legal action to enforce the agreement.

While it is not required to have a lawyer to create a Promissory Note, consulting one can be beneficial. A lawyer can help ensure that the note is properly drafted and complies with New York laws, which can prevent future disputes.

Yes, a Promissory Note can be modified if both parties agree to the changes. It is important to document any modifications in writing and have both parties sign the amended note to avoid confusion later.

If the borrower defaults on the Promissory Note, the lender has several options. They may pursue legal action to recover the owed amount, which could include filing a lawsuit. The specific actions depend on the terms outlined in the note and applicable state laws.

While both documents serve similar purposes, a Promissory Note is typically simpler and focuses primarily on the promise to repay a loan. A loan agreement, on the other hand, is more comprehensive and may include additional terms, conditions, and covenants related to the loan.