Free Promissory Note Form

Free Promissory Note Form

Electrical Panel Schedule Template - Lists GFCI and AFCI protected circuits for safety.

To begin your homeschooling journey in Washington, it's vital to understand the significance of the important Homeschool Letter of Intent details, as this document alerts the state of your educational plan for your children.

Media Release Form - A media release contains important details like the date and purpose of the media coverage.

Da31 Army - Instructions for completing the form can be accessed via a button on the document.

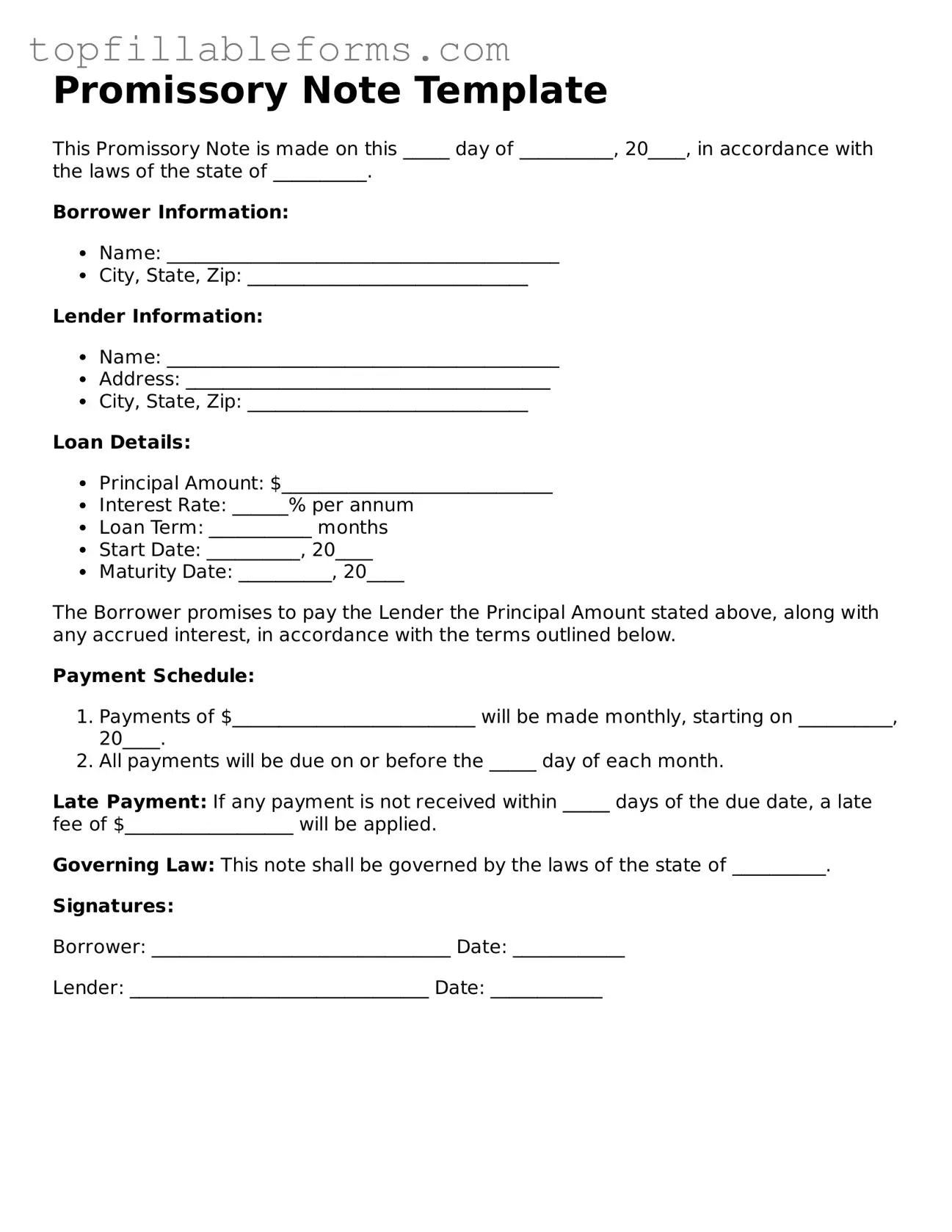

Promissory Note Template

This Promissory Note is made on this _____ day of __________, 20____, in accordance with the laws of the state of __________.

Borrower Information:

Lender Information:

Loan Details:

The Borrower promises to pay the Lender the Principal Amount stated above, along with any accrued interest, in accordance with the terms outlined below.

Payment Schedule:

Late Payment: If any payment is not received within _____ days of the due date, a late fee of $__________________ will be applied.

Governing Law: This note shall be governed by the laws of the state of __________.

Signatures:

Borrower: ________________________________ Date: ____________

Lender: ________________________________ Date: ____________

A Promissory Note is a vital document in any lending arrangement, serving as a written promise to repay borrowed money. When engaging in financial transactions, several other forms and documents may accompany a Promissory Note to ensure clarity and legal protection for all parties involved. Below is a list of commonly used documents that complement a Promissory Note.

These documents, when used in conjunction with a Promissory Note, help create a clear and legally sound framework for the lending process. Understanding each of these forms can empower both borrowers and lenders to navigate their financial agreements with confidence.

A Promissory Note is a financial document that outlines a promise to pay a specific amount of money to a designated party under agreed-upon terms. Several other documents share similarities with a Promissory Note. Here’s a list of six such documents:

Understanding the Promissory Note form is essential for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion and potential legal issues. Here are six common misconceptions:

Being aware of these misconceptions can help individuals navigate their financial agreements more effectively. Always consider consulting with a professional to ensure that your Promissory Note meets all necessary legal requirements and protects your interests.

A Promissory Note is a written promise to pay a specified amount of money to a designated person or entity at a defined time or on demand. It serves as a formal agreement between the borrower and the lender, outlining the terms of the loan, including the interest rate and repayment schedule.

Individuals and businesses often use Promissory Notes. They are common in personal loans, business financing, and real estate transactions. Anyone who borrows money or lends money can benefit from this document, as it provides legal protection and clarity regarding the terms of the loan.

A typical Promissory Note includes:

This information ensures that both parties understand their obligations and rights under the agreement.

Yes, a Promissory Note is a legally binding document. Once signed, it creates an obligation for the borrower to repay the loan according to the agreed-upon terms. If the borrower fails to make payments, the lender has the right to take legal action to recover the owed amount.

Yes, a Promissory Note can be modified, but both parties must agree to the changes. It is essential to document any modifications in writing and have both parties sign the updated agreement. This ensures that all parties are aware of the new terms and helps prevent misunderstandings in the future.