Attorney-Verified Promissory Note Template for Texas

Attorney-Verified Promissory Note Template for Texas

New York Promissory Note - It acts as an educational tool, helping borrowers understand their obligations and rights.

Proper documentation is vital when engaging in the sale of a trailer, as it not only protects both parties but also ensures compliance with local laws. For those looking to facilitate such transactions in New York, the nypdfforms.com/trailer-bill-of-sale-form provides a reliable resource for obtaining the necessary paperwork to formally document the sale and transfer of ownership.

California Promissory Note Requirements - A Promissory Note is a written promise to pay a specified amount to a designated person or entity at a later date.

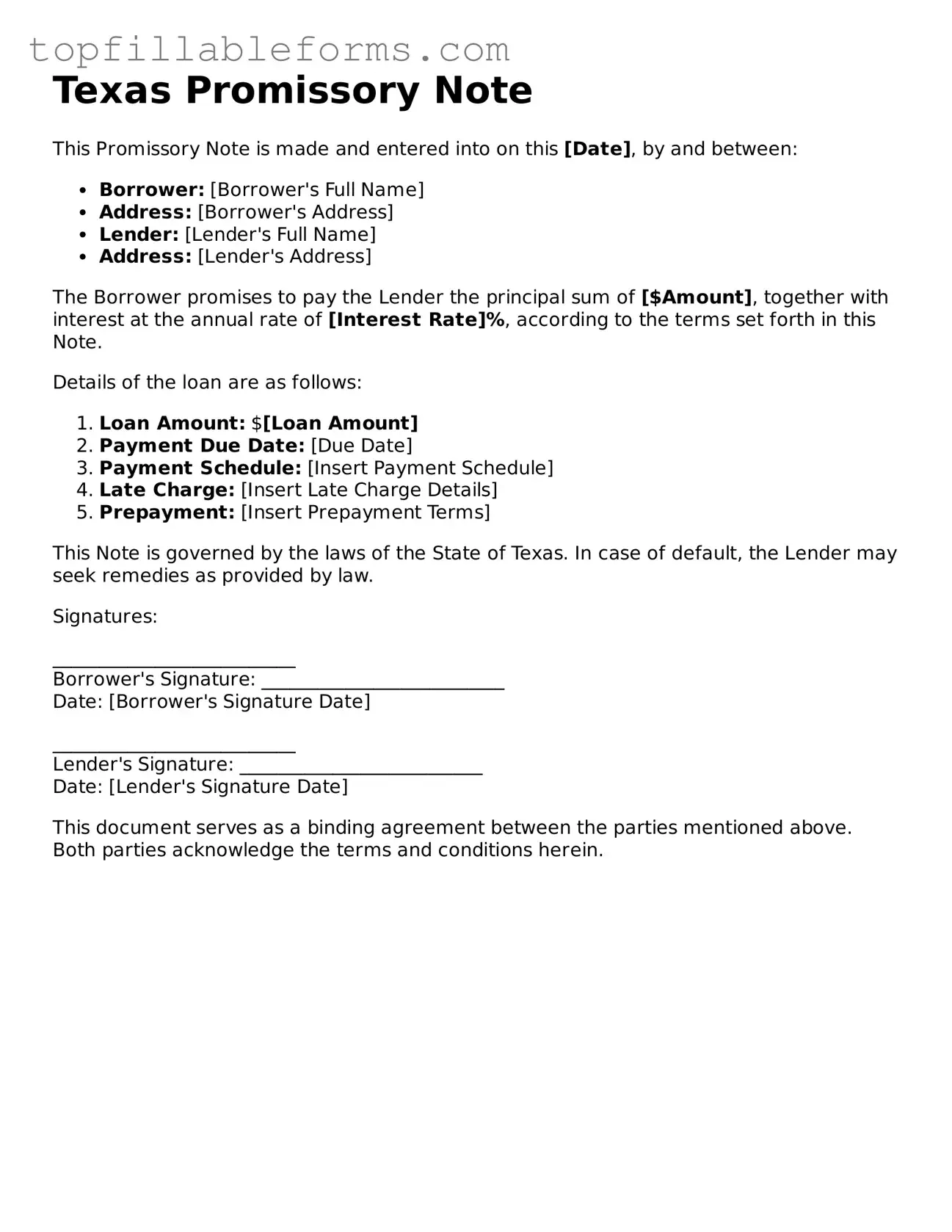

Texas Promissory Note

This Promissory Note is made and entered into on this [Date], by and between:

The Borrower promises to pay the Lender the principal sum of [$Amount], together with interest at the annual rate of [Interest Rate]%, according to the terms set forth in this Note.

Details of the loan are as follows:

This Note is governed by the laws of the State of Texas. In case of default, the Lender may seek remedies as provided by law.

Signatures:

__________________________

Borrower's Signature: __________________________

Date: [Borrower's Signature Date]

__________________________

Lender's Signature: __________________________

Date: [Lender's Signature Date]

This document serves as a binding agreement between the parties mentioned above. Both parties acknowledge the terms and conditions herein.

When dealing with a Texas Promissory Note, several other forms and documents may be necessary to ensure a clear understanding and proper handling of the loan agreement. Each of these documents serves a unique purpose in the lending process, helping both the lender and borrower establish their rights and responsibilities.

Understanding these additional documents can help both parties navigate the lending process more effectively. Each document plays a crucial role in protecting the interests of both the lender and borrower, ensuring that everyone is on the same page throughout the duration of the loan.

A Promissory Note is a financial document that outlines a promise to pay a specified sum of money to a designated person or entity under agreed-upon terms. While it serves its unique purpose, it shares similarities with several other important documents. Here are four documents that are similar to a Promissory Note:

Understanding the Texas Promissory Note form is crucial for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion and potentially costly mistakes. Here are eight common misconceptions about this important legal document:

Understanding these misconceptions can help ensure that both lenders and borrowers navigate the complexities of promissory notes more effectively. Clarity in these agreements is vital for protecting the rights and responsibilities of all parties involved.

A Texas Promissory Note is a written agreement in which one party promises to pay a specific amount of money to another party at a designated time or on demand. This document outlines the terms of the loan, including the interest rate, repayment schedule, and any penalties for late payments. It serves as a legal record of the transaction and can be enforced in a court of law if necessary.

Any individual or business can use a Texas Promissory Note when lending or borrowing money. This includes personal loans between friends or family, business loans, or any situation where one party needs to formalize a loan agreement. It is important for both parties to understand the terms and conditions outlined in the note before signing.

A Texas Promissory Note should include the following key information:

Including these details helps ensure clarity and reduces the potential for disputes in the future.

Yes, a Texas Promissory Note is legally binding as long as it meets certain requirements. The parties involved must have the legal capacity to enter into a contract, and the terms must be clear and specific. If a dispute arises, the note can be enforced in court, making it crucial for both parties to understand their rights and obligations under the agreement.